The U.S. Genius Act

...And the Bitcoin explosion

The Bitcoin has surpassed $120,000 which was considered a significant price barrier. Bitcoin investors are giddy with excitement. What has been different about the Bitcoin’s recent rally is that it seems to be fuelled, in part, by institutional demand - which has been surging on expectations that crypto will gain legitimacy as another arm of the economy, under the Trump presidency.

In January this year, we spoke about the new EU regulations on crypto. In June 2025, the U.S. Senate passed its own crypto bill, which is referred to as the Genius Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act). It still needs to clear the House of Representatives, but has already created sufficient buzz.

Similar to the EU’s MiCA regulations, the U.S. bill too seems to focus on stable coins (read the stable coins explainer & what has led to the popular usage of stable coins here). The Genius Act aims to restrict stablecoin issuance to certain federally regulated banks, qualified nonbank entities and state-regulated issuers under specified conditions.

With the Genius Act, all USD stable coins will need to be backed 1:1 by traditional asset reserves such as treasury bills and bank deposits. Those who were burnt in the collapse of Terra, will especially welcome this regulation. The liquidity & credit profile of the reserves has also been spelled out in the regulations, with consumer protection as the key theme of the regulation. It also mandates segregation of reserve funds vs. the issuer’s own funds, better transparency via reporting & audits, as well as stricter tracking of AML compliance.

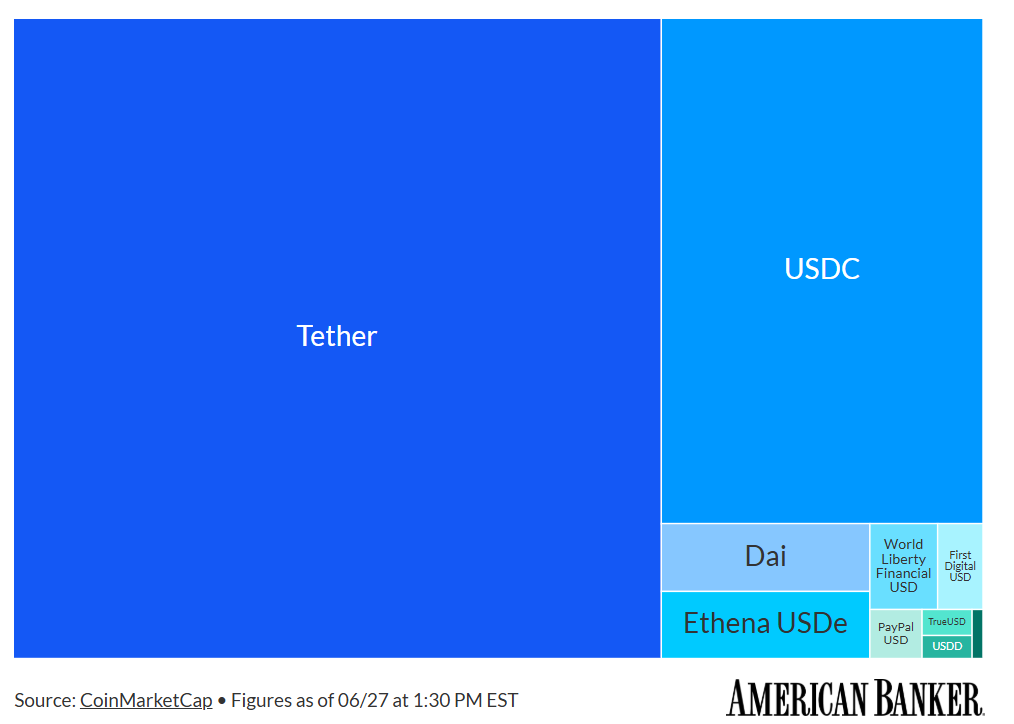

Some of the top U.S. banks, including Bank of America & JP Morgan, are considering teaming up to issue a common stablecoin. American banks are viewing this as a chance to improve the operational efficiency of transactions of course, but what does this mean for Tether, the current dominant player in the stable coins business?

Tether has long been reluctant to conduct audits or disclose fully its controversial reserve management practices. Foreign stablecoin issuers aiming to offer their stablecoins in the U.S. would need to comply with the requirement of technological capabilities to freeze, seize, or prevent transfers of their stablecoins based on lawful orders. If Tether is unable or unwilling to meet the new requirements, the USDC (the second largest stablecoin in the world), launched by Circle & Coinbase, has much to gain in terms of market share. On the other hand, stablecoins are popular because they are the dominant medium of exchange on blockchains. A Bank of America stablecoin could potentially wipe out all existing stablecoin issuers.

Overall, the bill could make stablecoins usage more popular within the financial system. For example, PayPal’s stablecoin PYUSD, which is being rolled out across its 20 million small & mid sized merchants, will gain legitimacy from this act. Amazon may be contemplating its own stablecoin - that could be a huge game-changer globally.

Circling back to the Bitcoin’s explosive surge though - how do regulations on stablecoins help Bitcoin, which is not a stablecoin? Let's think about the mandatory reserve rule. The stablecoin market is roughly $251 billion, set to double in value to $500 billion soon. At that scale, stablecoin issuers would be among the largest buyers of U.S. Treasury bills, utilizing the T-bills yield for coin redemptions. The coin issuers & their ecosystem could potentially become central to the U.S. financial system as a whole. The expectation therefore, is that crypto as a currency, as a medium of payment & as a industry will become more prominent. And this will drive institutional appetite for crypto tokens as a whole.

On the other hand, who knows, this Bitcoin rally could be yet another meme rally.

A last note: The U.S. administration is also hoping to pass the (i) Digital Asset Market Clarity Act (Clarity Act) - which aims to establish a comprehensive regulatory framework for digital assets and cryptocurrencies, and (ii) the Anti-CBDC Surveillance State Act which aims to block the issuance of a retail central bank digital currency (read here what CBDC is). These two upcoming acts deserve a separate post!